Naira Cards Resume International Transactions — What It Means in 2025

Yesterday a pair of customer emails from UBA and Wema landed like fireworks: Nigerian‐issued naira debit cards now work on Amazon, Netflix, POS terminals abroad, even foreign ATMs. Three years after the plug was pulled, the switch is on again.

Below is a friendly deep-dive into

-

Why the ban existed in the first place,

-

What changed this week, and

-

How the reopening reshapes the roadmap for virtual-dollar card startups, cross-border remittance players, and the broader fintech scene.

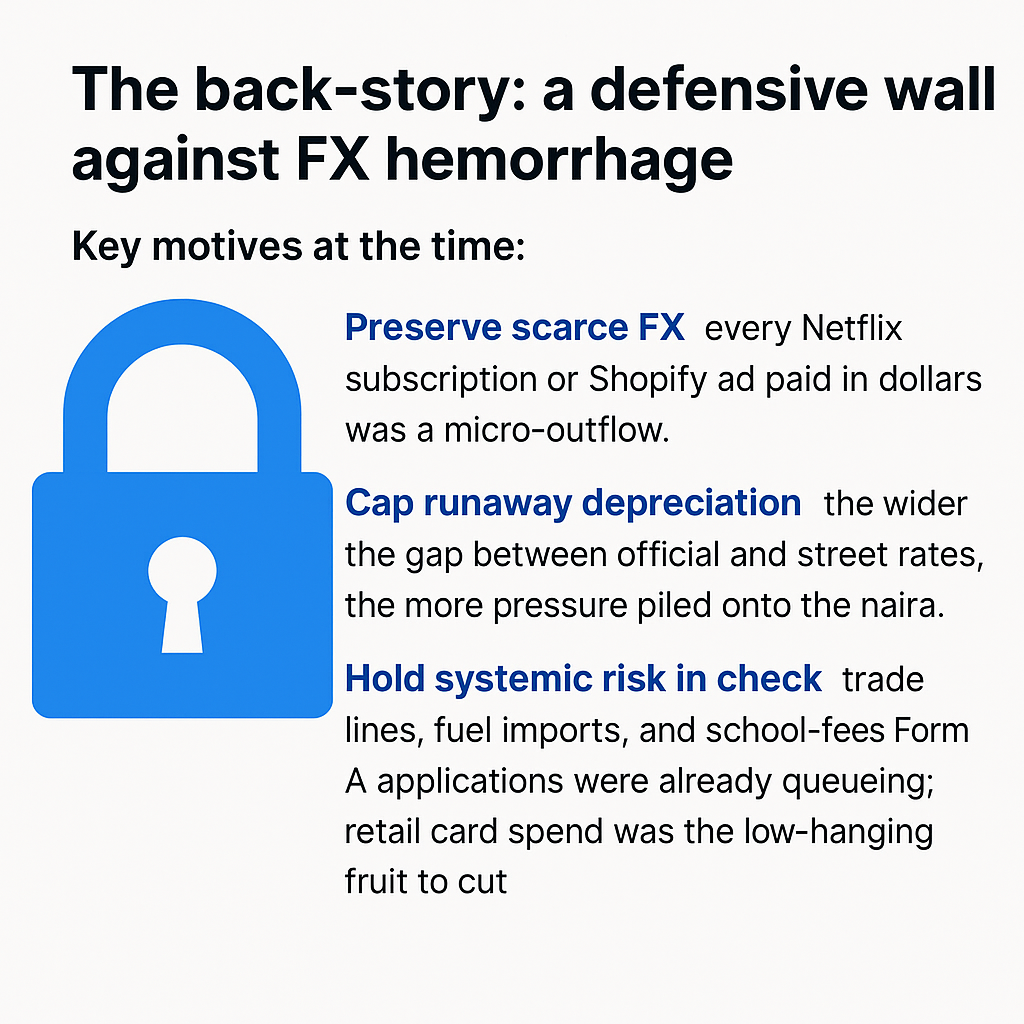

1. The back-story: a defensive wall against FX hemorrhage

By mid-2022 the Central Bank of Nigeria (CBN) was fighting a perfect storm: crude-oil earnings sagged, portfolio investors fled, and the parallel-market naira flirted with ₦900/$ while official windows sat nearer ₦450. To slow the leak in foreign reserves, banks began rationing dollars. Daily international spend limits first fell to $20, then several banks hit the red button altogether, suspending naira-denominated cards for overseas use. tribuneonlineng.compunchng.com

Key motives at the time:

-

Preserve scarce FX – every Netflix subscription or Shopify ad paid in dollars was a micro-outflow.

-

Cap runaway depreciation – the wider the gap between official and street rates, the more pressure piled onto the naira.

-

Hold systemic risk in check – trade lines, fuel imports, and school-fees Form A applications were already queueing; retail card spend was the low-hanging fruit to cut.

2. Why the green light now?

Several macro and policy shifts converged in 2024-25:

| Trigger | What changed | Evidence |

|---|---|---|

| FX liquidity bump | Oil receipts recovered and the CBN cleared part of its forward backlog, nudging average monthly inflows to almost $6 billion. | The Nation’s market recap thenationonlineng.net |

| Monetary reforms | The CBN unified multiple FX windows, floated the naira, and hiked interest rates, dampening demand for speculative dollars. | IMF 2025 Article IV note imf.org |

| Narrower parallel‐market premium | The street rate cooled below ₦1,000/$ for the first time in two years, reducing arbitrage upside. | BusinessDay analysis businessday.ng |

| Confidence signals from Tier-1 banks | UBA, GTBank, and Wema publicly re-enabled cards, each with modest quarterly caps ($500 – $1,000). | Guardian report and Nairametrics explainer guardian.ngnairametrics.com |

The card switch is partly a test balloon; caps remain tight and banks will monitor flows before opening the throttle.

3. Fintechs on the front line – disruption or opportunity?

a. Virtual-dollar card providers

Companies like Payday, Chipper Cash, Eversend, Grey, Cardtonic and others built their user bases on the very gap that just got smaller. Customers paid a mark-up (often ₦75-₦120 per dollar) in exchange for frictionless global payments.

-

Pressure on volumes: Some casual spenders will revert to their regular bank cards, especially if the bank’s FX rate plus fees undercut fintech spreads.

-

Higher-limit advantage: Banks are currently capping naira cards at $1,000 per quarter, while many fintech cards still allow $1,000 – $4,000 per month. Power users (ads, SaaS, travel) may stay put. nairametrics.com

-

Differentiation pivot: Expect fintechs to double down on perks like USD receiving accounts, multi-currency wallets, creator payouts, and cheaper P2P remittances rather than pure spending.

b. Cross-border payment and remittance startups

With traditional banks now slightly more competitive, fee compression is coming. Startups that offer instant settlement, better UX, or niche corridors (NGN-KES, NGN-GHS) still hold cards banks do not.

c. Banking-as-a-Service (BaaS) and embedded finance

More corporates will want in-app cards denominated in naira but accepted worldwide. Fintechs owning BaaS infrastructure can white-label this for creators, e-commerce stores, even neo-brokers.

d. Risk & compliance tech

Fraud monitoring gets tougher once tens of thousands of naira cards wake up on global rails overnight. Vendors in KYC, AML, and chargeback analytics could see a demand spike.

4. What should consumers expect next?

-

FX rate transparency – Banks must quote the exact rate at the point of transaction; hidden 5 percent mark-ups will push users back to fintechs.

-

Gradual limit lifts – If FX buffers hold, quarterly caps will creep upward, likely mirroring the $10,000 annual Personal Travel Allowance ceiling.

-

Competition on fees – Fintechs will slash card maintenance and funding charges; banks may answer with loyalty points or zero-fee foreign POS days.

-

More merchant acceptance – Some global platforms previously flagging Nigerian BINs as high risk will update whitelists, improving success rates.

5. How founders and product teams can stay ahead

-

Model multiple FX scenarios – stress-test margins at ₦800/$ and ₦1,200/$.

-

Bundle, don’t battle – pair virtual cards with dollar savings vaults or treasury bills to lock users in.

-

Invest in on-ramp UX – the easier it is to top up from local bank accounts or USSD, the stickier the product.

-

Lobby for smart regulation – engage the CBN fintech sandbox to shape forthcoming rules on digital wallets and capital controls.

Final thoughts

Yesterday’s switch flip is as much a signal as a service: policymakers believe liquidity is back, at least enough to let everyday Nigerians buy Coursera courses without a side-quest to find dollars. For fintechs, the sky is not falling but the terrain just changed. The winners will be those who treat cards as a feature rather than the whole product, layer value on top, and stay nimble in Nigeria’s ever-swinging FX weather.

Stay tuned—the next 90 days will reveal whether this is a temporary experiment or a lasting shift in Nigeria’s payment landscape.